USMCA Review: Possible Outcomes and Impacts for 2026

What follows is a Grok-heavy analysis of the current state of US-Canada trade relations, especially as there are only 3 months left until July 1 before USMCA sunset clause kicks in. As with my previous article on Canada-US history, the historical context is vital to understanding where we are headed. Grok served to digest the giant volume of data and commentary to provide a summarized picture of the current status of US-Canada trade, and what the possible outcomes are. My analysis and views follow at the bottom.

Current Status

The Canada–United States–Mexico Agreement (CUSMA in Canada, USMCA in the US, T-MEC in Mexico) entered into force on July 1, 2020, replacing NAFTA. There is no substantive difference between USMCA and CUSMA — they are identical legal texts with the same terms. The naming reflects national preference: USMCA puts the United States first, CUSMA puts Canada first in English, with ACEUM in French and T-MEC in Spanish.

The agreement includes a sunset mechanism under Article 34.7: it automatically terminates on July 1, 2036, 16 years after entry into force, unless each Party’s head of government confirms in writing that it wishes to extend for a new 16-year term. A mandatory joint review by the Free Trade Commission occurs on the sixth anniversary, July 1, 2026, and every six years thereafter if extended. If extension is not confirmed, the sunset clock activates: the Agreement remains fully in force, but annual joint reviews must be held until 2036, or until extended. Separately, any Party may unilaterally withdraw with six months’ written notice under Article 34.6.

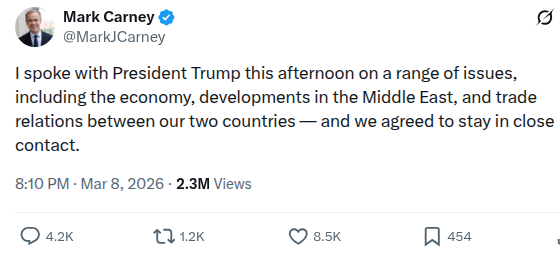

As of mid-March 2026, the review process is advancing. Domestic consultations are complete, and bilateral talks have begun. On March 5, 2026, USTR Jamieson Greer and Mexican Secretary of Economy Marcelo Ebrard launched formal US-Mexico bilateral discussions, with the first negotiator meeting scheduled for the week of March 16 (USTR press release). Canadian Minister Dominic LeBlanc met USTR Greer in Washington on March 6–7, describing talks as “constructive,” with dairy access explicitly raised (Reuters; Bloomberg). No full trilateral framework has started yet; the mandatory joint review still begins July 1, 2026. The atmosphere is tense and “bumpy,” with early bilateral momentum, especially US-Mexico, suggesting the U.S. may prioritize sequential deals.

President Trump has described the USMCA as “irrelevant” and offering “no real advantage” to the United States, stating variations of “we don’t need their product” and that it “wouldn’t matter to me” if it expired (Reuters; Wall Street Journal). He has privately mused about quitting the pact he signed and floated a bilateral US-Mexico deal that excludes or sidelines Canada. USTR officials have emphasized they are not prepared to recommend simple renewal without changes. The U.S. is using leverage — tariffs, including 2025 Section 232 adjustments and temporary 25% tariffs on Canada/Mexico that exempted most USMCA-compliant goods, keeping ~85% of trade duty-free, threats to block projects like the Gordie Howe bridge, and linkage to non-trade issues — to push for concessions on tighter rules of origin, especially auto to limit Chinese inputs, stronger protections against non-market economies, adjustments in dairy/supply management, digital trade updates, energy, and broader “America First” reindustrialization goals.

Canada sends approximately 75–80% of its total exports to the US, roughly 25% of Canadian GDP, making impacts highly asymmetric — the U.S. would experience minimal disruption in most scenarios. Economists from Oxford Economics, Scotiabank, Bank of Canada, Desjardins, CSIS, Brookings, and others have modelled scenarios. Likelihoods below reflect consensus from recent reports.

1. Renegotiated Deal with Targeted Changes + 16-Year Extension

Likelihood: ~45–55% (most probable baseline scenario)

The US secures concessions during post-July negotiations, likely concluding late 2026, leading to a revised or side-letter-amended agreement extended to 2042 (next review 2032). Changes focus on stricter auto rules of origin and labour-value content, enhanced safeguards against Chinese circumvention, modest additional US dairy & poultry access, and modernizations in digital trade or critical minerals. This allows Trump to claim a “win” while preserving integrated supply chains valued by US industries.

Detailed impacts on Canadian industries:

- Short-term negotiation uncertainty and compliance costs, followed by restored long-term stability and investment rebound.

- Automotive & Parts: This is a key Ontario sector. Moderate adjustment from tighter origin rules; higher compliance expenses or some production reallocation, but duty-free preferential access and dispute settlement preserved. Exports and employment largely maintained; limited plant closures.

- Energy: This is mostly Oil & Gas from Alberta, and makes up 30% of Canada’s U.S. exports. Minimal disruption as pipelines and exports continue under stable rules. Minor gains/losses depending on energy chapter tweaks.

- Agriculture: The supply-managed dairy and poultry sectors may concede slightly more U.S. quota access but retain core protections. Grains, meat, and oilseeds enjoy continued duty-free treatment with reduced retaliation risk.

- Forestry & Lumber: This is a key sector in BC, Quebec and Ontario. Softwood disputes managed through updated mechanisms; lower risk of escalating countervailing/anti-dumping duties.

- Mining & Metals: This is especially steel and aluminum but also other minerals. Section 232 tariffs likely exempted or moderated; $17B+ exports retain preferential status.

- Manufacturing: This includes machinery, chemicals, plastics, and non-auto products. Integrated supply chains preserved; prior CUSMA gains maintained.

- Textiles, Apparel & Footwear: Duty-free entry continues.

- Services, Digital Trade & Finance: Chapters on data flows, e-commerce, financial services, and temporary entry strengthened or upheld.

- Overall: Near-zero to slightly positive long-term GDP impact with a transition-year drag 0-0.3% GDP. Investment rebounds, Canadian dollar is stable, negligible recession risk.

2. No Extension Confirmed July 1 2026 – Sunset Clock Activates

Likelihood: ~30–35%

At least one Party, likely the U.S, declines written confirmation of the 16-year extension. Current rules remain intact, but annual reviews begin in 2027, creating sustained leverage through 2036. This creates prolonged uncertainty and fuels protectionism.

Detailed impacts on Canadian industries:

- General: Investment hesitation, delayed expansions, and hedging lead to gradual efficiency losses.

- Automotive & Parts: Caution in supply-chain planning; modest cost increases; minor production slowdowns but no immediate tariffs.

- Energy: Largely insulated; duty-free flows continue with planning uncertainty.

- Agriculture: Supply-managed stable; export commodities face planning friction and potential future retaliation.

- Forestry & Lumber: Elevated risk of softwood duties in annual talks, the mills continue to invest elsewhere.

- Mining & Metals: Section 232 remains a hovering threat.

- Manufacturing, Textiles, Services: Slower cross-border activity; digital/IP rules persist with reduced certainty.

- Overall: Cumulative GDP reduction 0.2–0.6% over years; unemployment +0.2–0.4 points; Canadian dollar weakens modestly. No immediate recession, but slower growth.

3. Fragmentation into Bilateral Trade Deals

Likelihood: ~10–15%

Trilateral breaks down, US pursues separate bilaterals, potentially favouring Mexico, while Canada relies more on WTO MFN, CPTPP, or diluted bilateral. Some elements survive bilaterally.

Detailed impacts on Canadian industries:

- General: Inconsistent rules raise compliance/logistical costs; supply chains fragment.

- Automotive & Parts: Disjointed origin rules increase costs and relocation pressure.

- Energy: Resilient but new bilateral frictions possible.

- Agriculture: Partial loss of duty-free for meat/grains; supply management preserved but exports shrink.

- Forestry & Lumber: Intensified disputes without unified settlement.

- Mining & Metals: Uneven steel/aluminum tariffs.

- Manufacturing, Textiles, Services: Erosion of digital trade, financial services, temporary entry; higher barriers for IT/consulting/finance.

- Overall: GDP loss 0.5–1.2% over 2–3 years; job losses concentrated in Ontario (auto) and BC/Quebec (forestry); slower recovery due to fragmentation.

4. Clean or Near-Clean 16-Year Extension

Likelihood: ~5–10% (possible if U.S. industry/Congress pressure prevails)

All three confirm extension with little substantive change — status quo plus minor technical updates.

Detailed impacts on Canadian industries:

- General: Highest certainty; full continuation of duty-free access, rules of origin, Chapter 19 dispute settlement, and modern chapters.

- All sectors: No new costs; predictability boosts investment, exports, and jobs. Energy and auto benefit most from integration.

- Overall: Positive GDP uplift ~0.3–0.8% from confidence; strongest employment/export performance; modest Canadian dollar strengthening.

5. Full US Withdrawal - Reversion to WTO + Higher Tariffs

Likelihood: ~5–10%

U.S. issues six-month notice or lets deal run out. Trade reverts to WTO most-favoured-nation tariffs, average ~1.7–2.5%, but higher in sensitive sectors. Plus possible use of Section 232 tariffs, 25% steel and 10% aluminum, and new “America First” measures. All CUSMA benefits such as rules of origin, Chapter 19, energy side letters, and digital rules disappear.

Detailed impacts on each Canadian industry

- Automotive & Parts: Worst hit. Just-in-time chains fracture. Loss of 75% regional/labour-value rules; 2.5% cars / 25% trucks return; Section 232 possible. Exports drop ~8.4% (>$5.6B), production ~5.5% decline, thousands of jobs lost. Plants may close/relocate.

- Energy:: Least affected. Most trade is already WTO duty-free; only minor diluent rules (~$60M/year) are lost. Pipelines continue; some volatility from retaliation.

- Agriculture: Mixed/net negative. Supply-managed (dairy/poultry/eggs) relatively better (U.S. loses extra quotas). Grains/meat/oilseeds/sugar: $21B+ exports face MFN + retaliation; meat especially hard-hit; farm incomes/production fall.

- Forestry & Lumber: Major disruption. No Chapter 19; softwood battles escalate. Countervailing/anti-dumping duties intensify + red tape. Mills slow; community job losses.

- Mining & Metals: Immediate severe. Section 232 snaps back; $17B+ affected. Other metals lose supply-chain certainty.

- Manufacturing: Chaos/delays/costs; chemicals/plastics lose $4B+ prior gains. Investment drops; capacity utilization falls.

- Textiles/Apparel/Footwear: High MFN (up to 32–35%) return; sharp production/job declines.

- Services/Digital Trade/Finance: Loss of data flows/e-commerce/financial/temporary entry chapters; new barriers for banks/tech/consulting/IT; IP weakens.

- Broader: Ripples to construction/retail/transport. ~38,000 direct industrial jobs at risk + secondary losses. GDP falls 0.6–1.9% in year one; unemployment 6.5–7.1%; recession probable in severe cases. The Canadian dollar weakens (some export relief, but inflation). Retaliation adds mutual pain with limited leverage. Businesses urged to diversify, stockpile, renegotiate contracts.

Overall for Canada in Outcome 5: Significant contraction/recession risk; U.S. barely notices aside from Auto and manufacturing where there is high cross-border integration.

Historical Parallel: Lessons from the Post-Civil War to 1910 High-Tariff Era

The risk of tariffs or disruption under potential USMCA withdrawal parallels the decades from the end of the American Civil War through to the beginning of WWI, when the US and Canada engaged in mutual high-tariff protectionism with limited reciprocity.

Tariff Levels

- United States: Protectionist period with average tariffs on dutiable imports at 40–50% via the Morrill extensions & McKinley Tariff in 1890, and Dingley Tariffs in 1897. Protected emerging manufacturing, especially steel & iron.

- Canada: Sir John A. Macdonald’s National Policy in 1879, raised average tariffs from 14% to over 21%, and many manufacturing tariffs to 30–50%. The goal was to shield growing industrial sectors, fund Canadian Pacific Railway, and promote east-west integration over north-south trade.

Impacts

- Trade was shallow and limited to raw materials and agriculture products from Canada, and finished manufactured goods from the US. Integration was minimal and goods crossed only once.

- The McKinley Tariff withheld reciprocity to pressure Canada into annexation. Canada retaliated on U.S. agriculture products, pivoted exports to Britain, and framed the 1891 election as resisting the US. Canadian nationalism strengthened and trade ties to the British deepened. Some US manufacturers built branch plants in Canada to bypass tariffs.

- Canada saw modest protected manufacturing growth, via Ontario & Quebec textiles & steel, but higher consumer prices and efficiency losses. Mark Twain called this period the ‘Gilded Age’ due to strong US growth.

Relevance and Comparisons to 2026

Similarities: US uses tariffs as leverage to protect its manufacturing sector. Canadians retaliate, adopt nationalist anti-US stance, and search for alternative trade partners.

Critical Differences — Why Modern Impacts Are More Severe:

- Dependence: Historical Canadian exports to the US were 35–60%. It was a relatively easy pivot to Britain, especially given how strong Britain was before WWI & WWII. Today Canada exports are 75–80% to the US and 25% GDP). This creates huge asymmetry that is exacerbated by weak alternatives. Britain and Europe in general are relatively weak compared to the pre-WWI period.

- Supply-Chain Integration: 19th-century arm’s-length commodities and one way flow of manufactured goods are in stark contrast to today’s just-in-time supply chain. Especially with intense vertical integration where auto parts cross the border 7–8 times. Tariffs and lost rules of origin multiply costs. The risks are immediate plant shutdowns and relocations, which did not happen in the previous period.

- Tariff Baseline: Historical tariffs were 40–50%. Today’s WTO MFN has a 1.7–2.5% average and targeted Section 232 tariffs at 10–25%. The shock today is driven more by breaking networks than tariffs alone..

- Speed/Scale: Historical effects were slow. Today’s modern models project 0.6–1.9% GDP loss and recession risk in year one, with +38,000 direct jobs threatened. This is amplified by capital mobility.

- Global Framework: There was no trade tariff floor historically; today there is some protection via WTO and low average MFN. The targeted 232 tariffs and uncertainty are still devastating.

Bottom-line Historical Lesson: Canada survived and partially industrialized under high tariffs via retaliation, diversification, and protected growth but at the expense of efficiency, growth and living standards. Today’s deeply integrated 2026 economy is far more vulnerable to sudden disintegration. Aggressive leverage can backfire politically and push partners toward alternatives rather than submission. However, there are very few feasible alternatives for Canada.

Additional Insights and Context (Mid-March 2026)

- Business Preparedness: Reports from the Canadian Chamber of Commerce and Boston Consulting Group urge Canadian companies to act now with contingency plans for extension with changes, prolonged uncertainty, or disruption. Actions include supply-chain diversification, inventory buffering, contract renegotiation, and exploring deeper ties with CPTPP/CETA partners. Even with ~60% of goods remaining duty-free in recent tensions, uncertainty chills investment.

- Geopolitical & Economic Security Focus: U.S. emphasis on reducing non-regional, especially Chinese dependence, strengthening rules of origin, and securing critical minerals/supply chains could lead to new chapters or side letters. Mexico’s business sector is 84% positive on USMCA and is pushing for modernization rather than full renegotiation.

- U.S. Domestic Angles: Some US industries and lawmakers are pushing for stability to protect jobs. USMCA supports millions of U.S. jobs, including 1.2 million in Texas alone. Labour groups seek stronger enforcement. Congress seeks more oversight, but the administration prefers flexibility.

- Risk of Backfire: Deep integration means disruption raises costs for US manufacturers and consumers too. Automakers and trade groups warn against exit or fragmentation.

- Long-Term Implications: Successful modernization could enhance North American competitiveness against global rivals via regulatory alignment, workforce mobility, and a joint agenda. Failure risks fragmentation that weakens all three economies. Prolonged uncertainty already weighs on Canadian investment and a renegotiated extension could reverse that.

- Political Signalling: For Canada, resisting overreach could reinforce national unity. For the U.S., visible “wins” serve domestic goals.

My Views

The above probabilities come from mainstream sources in Canada and the US. They are conservative by nature and use a balanced Canada US perspective. This radically downplays the asymmetry that this situation presents. As noted by Grok, the data states that the Canadian economy is directly dependent on the US for 75% of its exports, and 25% of its GDP. That is equivalent in size to the entire Canadian public sector.

The current US Administration has a strong America First mentality. And as they have shown all through 2025, they are not afraid to push their interests aggressively, especially when negotiating from a strong position. The US is aggressively pushing to reshore manufacturing and critical minerals. And it is aggressively looking to protect national security, especially at the border.

A weak Liberal government on the Canadian side has adopted a very defensive and adversarial approach to trade negotiations. And perhaps rightly so, as anything except a Clean Extension will hurt Canada. This exacerbates the asymmetry in favor of the US to an extreme. Scenario 4 - Clean Extension isn’t happening.

An important distinction that Grok made is that cross-border integration is vital for supply chains on both sides. And it noted the impact of tariffs is less vital than disintegration in the supply-chain, especially in auto and manufacturing. This integration and mutual co-dependence rules out Scenario 5 - Complete Withdrawal.

Interestingly enough Alberta is the least affected out of all of the provinces, regardless of outcome, due to WTO and CUSMCA terms around energy. Ontario is by far affected the worst, regardless of outcome except for a continuation of USMCA as-is.

Mexico has adopted a very constructive and positive approach to the USMCA review. And the rhetoric from both sides is very optimistic and oriented around partnership language. This again tips the asymmetry against Canada. If US-Mexico talks continue much more constructively leading up to July 1, this will be used as leverage against Canada. The most realistic worst-case outcome for Canada is Scenario 3 - Fragmentation into Bilateral Trade. This scenario results in Mexico receiving more favorable treatment than Canada. This is relatively unlikely as Canada would make heavy concessions to avoid this outcome.

Given what I know about America First and the extreme asymmetry in the relative Canadian and American positions, the July 1st deadline only 3 months away, I am very concerned for Canada. There is such radical asymmetry favoring the US position, and the rhetoric from both sides points to that. Add to that the general apathy of the Canadian public regarding this issue, and the general apathy of the American public to Canada in general. Over the next 3 months they need to find common ground, make rapid progress, tweak a few terms, and renew for another 16 years. The realistic best-case outcome for Canada is Scenario 1 - Renegotiated USMCA renewed by July 1. I personally find this highly unlikely even though Grok has this at 50%. It is Canada that is under the clock here, not the US. And without Canada speeding things up, this just isn’t going to happen. This outcome requires Canada radically change its approach and pivot to a more friendly stance, which there is no evidence of at all.

Which leaves us with Scenario 2 - No Extension Confirmed July 1 2026 – Sunset Clock Activates. I view this as the most likely outcome, far greater than 50%. This outcome leverages the US position more heavily against Canada. Current cross-border integration would continue protecting American interests. Missing the July 1 deadline will hurt Canada more than the US, adding to the uncertainty surrounding the Canadian economy and general direction of the country. And it will weaken their resolve in resisting the asymmetric position the US is pressing. It is quite likely that Canada will be more willing to make more serious concessions after July 1st. Pressure from Canadian industry would increase on Canada, especially the longer the uncertainty is prolonged through 2026. This outcome heavily favors the US, but it fits well with the strength from which the US is negotiating.

Canada is not likely to see the USMCA continue as-is. This review has already hurt the Canadian economy due to the gulf in rhetoric from both sides, by increasing economic uncertainty, and it will do more damage unless Canada pivots to a more America First friendly stance. I was already positioned to avoid Canada’s current economic doldrums, and I plan to continue to deploy capital elsewhere. Aside from Alberta oil and gas, there are no Canadian sectors that are protected from, let alone benefit, from ongoing USMCA issues.